RENAISSANCE JEWELLERY – UNDERVALUED FOR A REASON

“India is the second largest jewellery market in world after China”

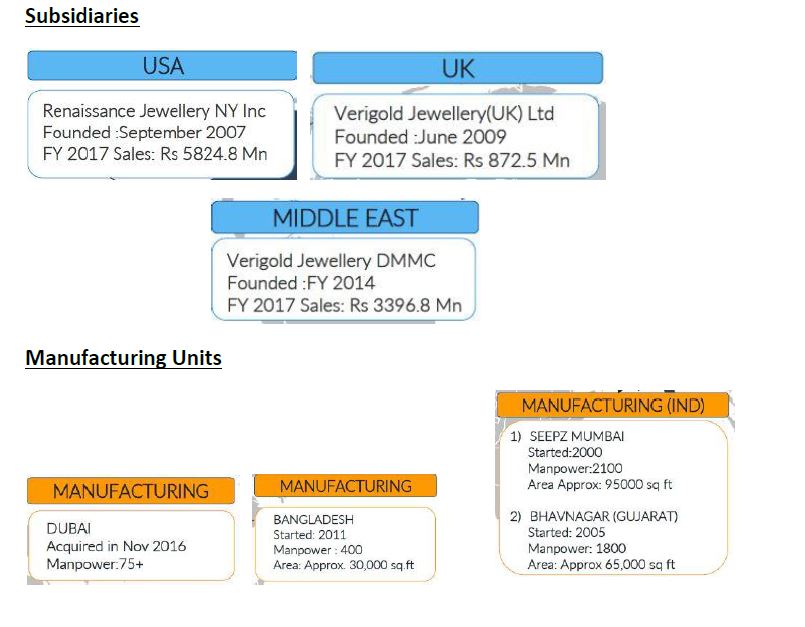

Renaissance Jewellery is engaged in business of design, manufacturing, and sales of various types of jewellery. Company has wholly owned subsidiaries in US, UK, Dubai, to facilitate its sales and operations globally. This Mumbai-based company is mainly involved in designing and manufacturing low-priced products for brands like Amazon, JCPenney, Walmart in the overseas markets. It also has a licensing tie-up with Hallmark. thereby reducing the risk of dependence on a few clients.

Products

Jewellery products include rings, pendants, earrings, bracelets, necklaces & bangles. Design of these products is centralized in Mumbai and manufactured in three facilities - Mumbai, Bhavnagar & Bangladesh with total area of 1,90,000 sq ft engaging around 4000 manpower.

Value Migration from un organized to organized

Massive value migration taking place in Indian Jewellery industry with more than 70% (largest share in unorganized segment) shift from un organized to organized. Strict norms by govt such as Levy Of 1% exise duty on gold jewellery and implementation of 3% GST have permanently dented the advantage that unorganized players were enjoying, there by making things bright for listed high quality jewellery players. So, a sector that can’t be ignored.

FINANCIALS

Renaissance Jewellery is an established jewellery maker with international quality standard and has grown steadily in terms in Sales and profits in the last few years.

This value migration was evident from the stellar Q2 results published by RJL.

Going forward Management expects consolidated sales to grow by 18 to 22% and PAT to grow by 40-50% over FY 17.

Renaissance Jewellery made a cash offer to buyback upto 2 lakh fully paid equity sahres of the company at price of Rs 250/- per share aggregating to 5 crore. This instils confidence among investors when management buying and increasing stake from open market . The company exhibits financial discipline, efficient cost structure and risk controls, constantly improving product mix and focus on operating margin. This has helped Renaissance grow its sales by nearly 40% in the last three years to Rs 1,320 crore and more than treble its net profit to Rs 48 crore.

Peers Comparision

Geographical Diversification

USA continues to remain the main market for the company in jewellery business. Over the last 6 years sales to USA as proportion has reduced. Sales in the Middle East will take the second slot and is expected to be more than 25% of the consolidated sales going forward. This is likely to reduce the seasonality in sales to some extent. Over the years, the company has gradually shifted from gold to silver — from 70% in 2010, gold now accounts for 30%. Through its innovation and designing team of more than 200 people, the company has managed to keep strong negotiation power with clients. Most of its sales is generated in the second half of the fiscal due to Christmas and Valentine's Day.

CONCERNS

Contingent liability

Company has not made any provision for a contingent liability of 213 crore, for a matter pending in Bombay High Court, from commissioner of customs, alleging that the import of finish jewellery for remaking is not a permitted activity for an unit in SEZ, and hence chargeable to Custom Duty. Any adverse impact in this case would substantially erode the reserves of the company there by resulting in lowering of book value and making valuations different from current scenario. A prime reason for which this company is not getting high discounting like its peers. But this fact is known to the market, and considering management buyback at Rs 250/- company earnings outlook is very positive going forward. However this remains a substantial risk for the company, in coming years. This is one of the major reason why the company is available cheap, if not the case then it would have quoted much higher.

Conclusion

If the company is able to walk the talk and maintain the sales and profitability growth as projected, then the current valuations are a mockery, it will demand much higher valuations going forward. However investors must take into account the risk of contingent liability before investing in the company.

N.B- This article is for knowledge purpose, investors and members are required to take their own decision after thorough research. I am an investor at these levels after analyzing all bells and whistles of the company.

Hey, thanks for the information. your post s are informative and useful.

ReplyDeleteSuratwwala IPO